-

Panic and Run!

When my daughter was young her favorite show was a Disney cartoon called “The Lion Guard.” In one episode, the Lion Guard was trying to help a zebra whose herd was under attack by some hyenas, and the zebras’ reaction was to panic and run. I can still see my daughter dancing around the house singing, “Panic and run, panic and run!” – which also describes the markets in the first quarter. From the first attacks on Iran on February 28, the S&P 500 fell approximately 5 percent by quarter end. On February 27 (the day before the attack), the ten-year U.S. Treasury had a yield of 3.97 percent, and it rose to 4.32 percent by quarter end. So, investors were selling stocks, and they were selling bonds. The German Bund had a yield of 2 percent on February 27 and finished at 3.01 percent. Gold was $5,230 per ounce the day before the attack and ended the quarter $4,586 an ounce. Should I keep going? In times of crisis, all correlations go to one. Diversification is important in the long-run, but it is not a silver bullet. Sometimes the best way to handle a storm is to go through it; knowing what we own and why we own it gives us the confidence to do it.

To read the full report, please download the PDF.

~First Quarter 2026

-

Diversification

For casual market followers, it may seem as if we are in one continuous bull market. However, the market continues to shift below the surface. This past quarter healthcare stocks were up 11.7 percent while the technology sector was up only 1.4 percent. The techdriven market of the last 15 years has finally given way to diversification. Emerging market stocks were the best place to be in 2025, followed closely by developed international stocks. Commodities have gone sky high with gold over $5,000 per ounce, and silver has been on an even bigger run. AI is impacting everything. On a weekly basis, we run attribution on our own core equity strategy. At one point in December, the best five stocks were all technology, and the worst five stocks were also technology. On the whole, we had a slight underweight to technology, so it is not as if this is the only area in which we are invested. The key takeaway is that we are in an environment where diversification is not only working, but necessary.

To read the full report, please download the PDF.

~Fourth Quarter 2025

-

Voting or Measuring

“In the short run the market is a voting machine, but in the long run, it is a weighing machine.”

– Benjamin Graham

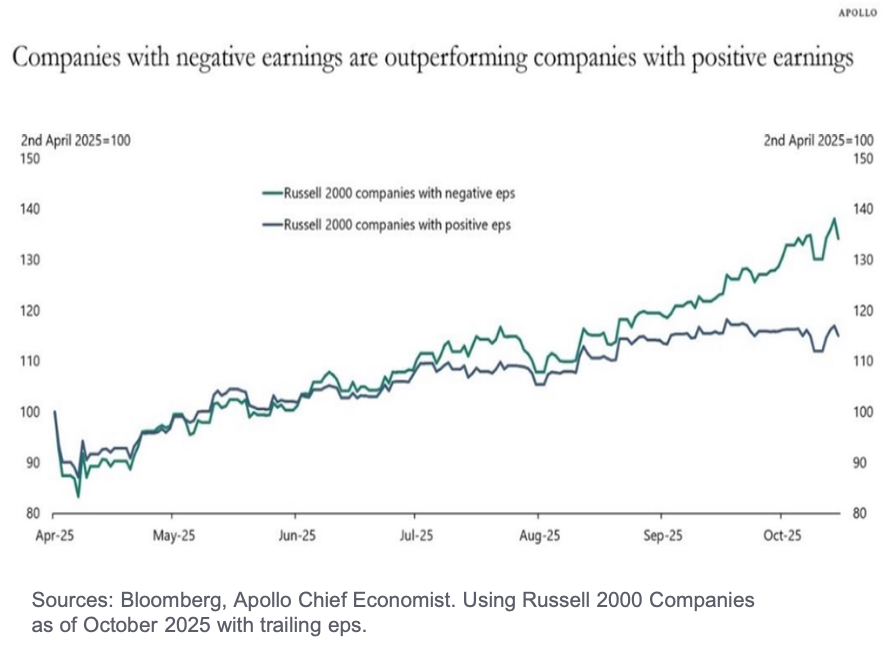

There is a great deal of wisdom in this famous quote. However, like many wise words they are far easier to say than to live by. No one likes to see a fund manager underperforming over a quarter and when they do, we immediately believe they have done something wrong. Often however it is the market not the manager that has temporarily lost its way. According to Bloomberg as of October 2025 inside the Russell 2000 there are 1120 companies with positive earnings per share and 806 had negative earnings per share. Since the downturn in April the companies with negative earnings are up over 30 percent while the ones with positive earnings are up a little more than 10 percent. The market is in voting mode, while we prefer managers who weigh things. Patience is in order.

To read the full report, please download the PDF.

~Third Quarter

-

In Defense of Freedom

Freedom is under attack from seemingly all directions today. Voters in New York just selected a socialist in the democratic primary. Vice president JD Vance recently admonished conservatives who he claims, “worship the capital M market.” Milton Friedman famously observed that, “Underlying most arguments against the free market is a lack of belief in freedom itself.”

This still holds true, but today there is another element from those who lack understanding of what the term “free market” means.

Today we hear the line that “the free-market economy is not working for everyday people.” We hear this from both the left and the right. However, every single example they give is, without fail, a place where regulation has replaced the free market. The greatest pain points (housing, higher education, and healthcare) are all areas where we long ago abandoned a free market approach.

Freedom isn’t free, and we too often forget how rare it is in human history. We need to do a better job of educating. The emphasis in free market is on free.

To read the full report, please download the PDF.

~Second Quarter 2025

-

Perception v. Reality

What we perceive and what is real are not always the same. One of the main arguments for tariffs is that we need to bring back the good blue-collar jobs that have been lost by deindustrialization. No one could possibly argue against this, if only it were factual. Here are the facts: U.S. manufacturing output as a percentage of real GDP has varied only 2% (13% – 11%) since 1947, according to the St. Louis Fed.

According to data from the U.S. Bureau of Labor Statistics (BLS), manufacturing employment peaked in 1979. Since that time, we have lost 6.7 million manufacturing jobs, and we have gained 9.4 million jobs in trade, transportation, and utilities. So, for every manufacturing job that has been lost since 1979, 1.4 jobs have been created in trade, transportation, and utilities, yet no-one talks about it.

Finally, there are more automotive manufacturing jobs in America today then there were in 1993 when Bill Clinton signed NAFTA. According to the BLS, there are 308,000 jobs today versus 298,000 at the peek of the 1990s. Does that surprise you?

To read the full report, please download the PDF.

~First Quarter 2025