![]()

Iron Capital’s quarterly investment newsletter through which we share our views on investing your assets in the current market environment.

Yeast is a very small thing, but the difference it makes in bread is huge. In the institutional retirement plan world, there is very little difference between doing the right thing for plan participants and covering one’s behind – DTRT or CYA? The difference in action is no bigger than a single grain of yeast, but oh my what a difference it makes in outcomes.

We have just experienced one of the strangest quarters that I can remember. At the beginning of June, Goldman Sachs research indicated that all of the return for the S&P 500 year-to-date through May was attributed to just seven stocks; the other 493 stocks in the S&P 500 have an average return of zero, nada, zilch. How did that happen?

The economy is hanging in there better than most experts suggest, since rising interest rates are not actually stopping consumers from living their daily lives. We maintain our view that we will either escape a recession all together or have a very mild one. We are not basing that on our business, but on feedback we get from others. Let’s take a look.

In the 30+ years I have been in this business, I do not recall a time when so many were so convinced that a recession was inevitable… which is precisely why I doubt a severe recession will occur this year. The economy flows in a way not dissimilar to nature. Nature has its seasons, the economy has the business cycle; the difference is human psychology.

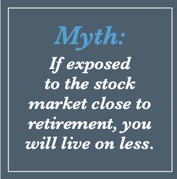

For as long as I can remember, there has been a myth that investors must reduce their exposure to stocks and increase their exposure to bonds as they approach retirement. This advice is based on the fallacy that if one is exposed to the stock market and we have a bear market (as we do today) at or close to one’s retirement, then his retirement will be forever impacted. That is wrong.

Myths die hard. For as long as I can remember, there has been a myth that investors must reduce their exposure to stocks and increase their exposure to bonds as they approach retirement. This advice is based on the fallacy that if one is exposed to the stock market and we have a bear market (as we do today) at or close to one’s retirement, then his retirement will be forever impacted. He will have to live on less and suffer for his bad timing.

That is wrong. It is wrong in lots of ways, but most importantly it ignores a far greater risk: outliving one’s resources. In the 30 years I have been in the investment business, primarily focused on retirement, I have seen four huge mistakes that need to be avoided at all costs. The first is taking too much risk when one is young, then panicking and selling everything during a bear market. We talk about this often.

The second is retiring without a plan. I am not talking about a financial plan; I mean an action plan. What are you going to do that will take up your time and fill your life with meaning? If you do not know the answer to that question, then you are not ready to retire. Vacations are great, but they are largely great because they are short. If one retires at age 65 today, then she is likely to be in retirement for 25 or 30 years. One can only play so much pickleball. She had better have a plan as to what will keep her active and engaged with others. The third mistake is outliving one’s health. Modern medicine is designed to keep one from dying, and they have gotten really good at it. That, however, is not the same as living. The more I deal with retirees, the less I care how long I live. I just want to really live right up until the end. Even if you have never exercised in your life up to retirement, you had better start, because your ability to physically function is a use-it-or-lose-it skill.

The fourth mistake is the one we will deal with in this article: becoming too conservative at or in the decade or so before retirement. This leads to outliving one’s resources, and if there is anything as horrible as outliving one’s health, this is it. The risk of outliving one’s resources is the risk that investors should think about the most. It dwarfs the risk of market volatility, yet that is what most people think of as risk. Most people look at what has happened to the market this year and think, “This is risk; this is the scary part.”

It is human nature. We know better, but it is difficult to see the current value of one’s investments drop and not be anxious about it. That is a normal reaction, but we have to remind ourselves that this is part of the cycle of life. We see ups and downs, and the ups will outweigh the downs over time as long as we stay the course. Time is on our side. Since 1926, the S&P 500 has been up 72 percent of the time. We get a negative year on average once every four years. This will pass, and the market will go to new highs.

This truth leads to one of the fallacies that causes people to hit the brakes too soon. They say, “If you are young then you have time to recover, but if you are about to retire, then you do not.” Wrong! This is the fallacy of the wrong time horizon. An investor who is investing for her retirement does not have a time horizon that ends on her retirement date; her time horizon is her life expectancy, which today is at least 20 years after retirement. I use 20 because when I was an economics student, we learned that as far as mathematical projections go, 20 years equals infinity. Anything beyond that time period is pure garbage. In our investment policies, the longest time horizon one can have is 20+ years, and one has that time horizon into their 70s.

How did the idea of retirement as an end date ever get started? Unfortunately, that has to do with the evolution of the investment industry and the incredible difficulty the industry has in serving investors through retirement. Many years ago, investors either did it themselves or hired an investment adviser to manage their money for them. Either way, all the actual transactions had to go through a broker. In fact, to simply know what was happening in the market that day one had to go to a “wire house” brokerage firm. These were the large New York-based broker-dealers who would pay the expense of having a wire service run to their regional offices around the country.

These firms had brokers in all of these offices because the only way to transact was in person. Technology has replaced that entire system. If your phone has a cell signal, then you can know what is happening and can trade stocks. In most businesses this would have meant the end of the broker, and in my opinion it should have. However, in the investment business, the broker transformed himself into the financial adviser. The broker’s historical role was that of a salesperson. If his broker-dealer had stock of GE, then he would be selling GE that day. The next day they might have a bond from GM, and he would sell that.

The role has not really changed, but most people today are not interested in paying the high cost of buying a stock or bond from the salesperson when they can do it far more efficiently online. Today the financial adviser sells money management; unfortunately, he isn’t a money manager. However, this works for most money managers, because they frankly are more comfortable looking at spreadsheets than talking to people. They can manage money the way they want and turn it into a product that gets sold by financial advisers, who are generally good with people.

Hence, the money management industry evolved from a service profession to a product manufacturing business. The brokerage business evolved from selling stock and bonds to selling managed products. This is far from ideal in our opinion, but it does work for accumulating resources. The vast majority of the products sold by advisers are geared toward growing one’s investments, so while a truly tailored approach is not possible, it is possible to build a portfolio of products that will grow in value over time.

The problem comes when one retires and transitions to producing income. While everyone who is still in the accumulation phase can be oversimplified as needing to make money, each person in the income phase has a truly unique situation. Designing a product for that is like trying to fit a square peg into a round hole – it simply will not work.

The third mistake is outliving one’s health. Modern medicine is designed to keep one from dying, and they have gotten really good at it. That, however, is not the same as living. The more I deal with retirees, the less I care how long I live. I just want to really live right up until the end. Even if you have never exercised in your life up to retirement, you had better start, because your ability to physically function is a use-it-or-lose-it skill.

The fourth mistake is the one we will deal with in this article: becoming too conservative at or in the decade or so before retirement. This leads to outliving one’s resources, and if there is anything as horrible as outliving one’s health, this is it. The risk of outliving one’s resources is the risk that investors should think about the most. It dwarfs the risk of market volatility, yet that is what most people think of as risk. Most people look at what has happened to the market this year and think, “This is risk; this is the scary part.”

It is human nature. We know better, but it is difficult to see the current value of one’s investments drop and not be anxious about it. That is a normal reaction, but we have to remind ourselves that this is part of the cycle of life. We see ups and downs, and the ups will outweigh the downs over time as long as we stay the course. Time is on our side. Since 1926, the S&P 500 has been up 72 percent of the time. We get a negative year on average once every four years. This will pass, and the market will go to new highs.

This truth leads to one of the fallacies that causes people to hit the brakes too soon. They say, “If you are young then you have time to recover, but if you are about to retire, then you do not.” Wrong! This is the fallacy of the wrong time horizon. An investor who is investing for her retirement does not have a time horizon that ends on her retirement date; her time horizon is her life expectancy, which today is at least 20 years after retirement. I use 20 because when I was an economics student, we learned that as far as mathematical projections go, 20 years equals infinity. Anything beyond that time period is pure garbage. In our investment policies, the longest time horizon one can have is 20+ years, and one has that time horizon into their 70s.

How did the idea of retirement as an end date ever get started? Unfortunately, that has to do with the evolution of the investment industry and the incredible difficulty the industry has in serving investors through retirement. Many years ago, investors either did it themselves or hired an investment adviser to manage their money for them. Either way, all the actual transactions had to go through a broker. In fact, to simply know what was happening in the market that day one had to go to a “wire house” brokerage firm. These were the large New York-based broker-dealers who would pay the expense of having a wire service run to their regional offices around the country.

These firms had brokers in all of these offices because the only way to transact was in person. Technology has replaced that entire system. If your phone has a cell signal, then you can know what is happening and can trade stocks. In most businesses this would have meant the end of the broker, and in my opinion it should have. However, in the investment business, the broker transformed himself into the financial adviser. The broker’s historical role was that of a salesperson. If his broker-dealer had stock of GE, then he would be selling GE that day. The next day they might have a bond from GM, and he would sell that.

The role has not really changed, but most people today are not interested in paying the high cost of buying a stock or bond from the salesperson when they can do it far more efficiently online. Today the financial adviser sells money management; unfortunately, he isn’t a money manager. However, this works for most money managers, because they frankly are more comfortable looking at spreadsheets than talking to people. They can manage money the way they want and turn it into a product that gets sold by financial advisers, who are generally good with people.

Hence, the money management industry evolved from a service profession to a product manufacturing business. The brokerage business evolved from selling stock and bonds to selling managed products. This is far from ideal in our opinion, but it does work for accumulating resources. The vast majority of the products sold by advisers are geared toward growing one’s investments, so while a truly tailored approach is not possible, it is possible to build a portfolio of products that will grow in value over time.

The problem comes when one retires and transitions to producing income. While everyone who is still in the accumulation phase can be oversimplified as needing to make money, each person in the income phase has a truly unique situation. Designing a product for that is like trying to fit a square peg into a round hole – it simply will not work. It also leads to the idea that when one retires, she must take all her money and put it into an income-producing product. If one did that, then the balance of the portfolio on the day of retirement becomes extremely important. If the investment industry is just a product-pushing business, then the timing of switching products becomes much more important than it should be.

At Iron Capital, we do not believe that the industry should be about pushing products. We believe it is supposed to be a professional service. As such, we build each income-producing portfolio from the bottom-up, tailored to each client’s needs. Our philosophy is simple: Build a portfolio that generates the income needed while taking as little risk as the market will allow.

We have been in a historically low-interest-rate environment for most of the last 20 years, certainly since the financial crisis in 2008. This hurts most income-focused products because they primarily invest in bonds. Bonds, after all, are simply loans. The loans are paid back plus interest, which produces income. The industry has really struggled in trying to solve the retirement income puzzle in this environment. For the most part, they just gave up and started telling their clients that they would have to live on less.

Article after article preached the demise of the so-called 4 percent rule – the “rule” that one could only take 4 percent of their portfolio as income if they wished to preserve the capital. In the meantime, most of our clients need closer to 6 percent. The product-based solutions are no solution at all. We have delivered the income our clients need by taking the best income sources available at the time. For most of the last 20 years that has meant dividend-paying stocks, preferred stocks, and higher-yielding bonds.

The good news is that while we have more in stock, the stocks we were investing in for these clients are more conservative. They tend to hold up extremely well during market downturns. The one exception to that rule was the Covid shutdown. These conservative companies that pay dividends tend to do well in thick or thin, but not when the government says you have to shut down. So, what did we do?

We put enough in safe places to pay the income needs for a few years, and then took advantage of the silver lining of the downturn. Every bear market creates opportunity. We took advantage of that opportunity to rebuild our client’s income portfolios. This is also what one should do when retiring in, or shortly after, a bear market.

When producing the needed income is a professional service and not a product, one gains flexibility. There is no need to have a one-time flip of the switch; the transition into retirement is exactly that – a transition. There is no rush, as we are going to be managing the income production for 20 to 30 years, if not longer. There is no need for a bear market at one’s retirement to be any different than a bear market at any other time.

Today we are in a bear market, and it is creating opportunities. For the income-needing client, those opportunities are now in bonds. For the first time in a very long time, bonds are paying enough interest to be a meaningful portion of an income strategy. This, however, is not going to help the product pushers. Bonds are simple: One loans his money to a company or government, and the borrower promises to pay it back plus interest. If one buys a bond, then she will get interest payments, and at maturity, the return of her principal. There is a risk that a borrower will not be able to pay it back, but that risk can be judged up front.

Bond funds, i.e. the products, do not work that way. What one is really doing is buying shares in a mutual fund. The fund then invests in bonds. Should interest rates rise further, the bonds will lose value in the market. A bondholder who isn’t selling doesn’t care, because she will continue to get what she agreed to from the beginning. The bond fund, however, will lose value. It does not behave like an actual bond; it behaves like a mutual fund that happens to invest in securities with lower return potential.

Retirement is a personal experience. It is a stage of life, not something one buys from a store. Managing one’s investment portfolio to produce the needed income is just as personal and just as unique. If one wishes to go the product route, then he had better have saved a lot of money and avoided the last-minute downfall. On the other hand, if one goes the route of professional service, then she will be able to navigate life’s ups and downs with far more flexibility. Bear markets are horrible to endure, but they do produce opportunities – even for those about to retire.

Warm regards,

It also leads to the idea that when one retires, she must take all her money and put it into an income-producing product. If one did that, then the balance of the portfolio on the day of retirement becomes extremely important. If the investment industry is just a product-pushing business, then the timing of switching products becomes much more important than it should be.

At Iron Capital, we do not believe that the industry should be about pushing products. We believe it is supposed to be a professional service. As such, we build each income-producing portfolio from the bottom-up, tailored to each client’s needs. Our philosophy is simple: Build a portfolio that generates the income needed while taking as little risk as the market will allow.

We have been in a historically low-interest-rate environment for most of the last 20 years, certainly since the financial crisis in 2008. This hurts most income-focused products because they primarily invest in bonds. Bonds, after all, are simply loans. The loans are paid back plus interest, which produces income. The industry has really struggled in trying to solve the retirement income puzzle in this environment. For the most part, they just gave up and started telling their clients that they would have to live on less.

Article after article preached the demise of the so-called 4 percent rule – the “rule” that one could only take 4 percent of their portfolio as income if they wished to preserve the capital. In the meantime, most of our clients need closer to 6 percent. The product-based solutions are no solution at all. We have delivered the income our clients need by taking the best income sources available at the time. For most of the last 20 years that has meant dividend-paying stocks, preferred stocks, and higher-yielding bonds.

The good news is that while we have more in stock, the stocks we were investing in for these clients are more conservative. They tend to hold up extremely well during market downturns. The one exception to that rule was the Covid shutdown. These conservative companies that pay dividends tend to do well in thick or thin, but not when the government says you have to shut down. So, what did we do?

We put enough in safe places to pay the income needs for a few years, and then took advantage of the silver lining of the downturn. Every bear market creates opportunity. We took advantage of that opportunity to rebuild our client’s income portfolios. This is also what one should do when retiring in, or shortly after, a bear market.

When producing the needed income is a professional service and not a product, one gains flexibility. There is no need to have a one-time flip of the switch; the transition into retirement is exactly that – a transition. There is no rush, as we are going to be managing the income production for 20 to 30 years, if not longer. There is no need for a bear market at one’s retirement to be any different than a bear market at any other time.

Today we are in a bear market, and it is creating opportunities. For the income-needing client, those opportunities are now in bonds. For the first time in a very long time, bonds are paying enough interest to be a meaningful portion of an income strategy. This, however, is not going to help the product pushers. Bonds are simple: One loans his money to a company or government, and the borrower promises to pay it back plus interest. If one buys a bond, then she will get interest payments, and at maturity, the return of her principal. There is a risk that a borrower will not be able to pay it back, but that risk can be judged up front.

Bond funds, i.e. the products, do not work that way. What one is really doing is buying shares in a mutual fund. The fund then invests in bonds. Should interest rates rise further, the bonds will lose value in the market. A bondholder who isn’t selling doesn’t care, because she will continue to get what she agreed to from the beginning. The bond fund, however, will lose value. It does not behave like an actual bond; it behaves like a mutual fund that happens to invest in securities with lower return potential.

Retirement is a personal experience. It is a stage of life, not something one buys from a store. Managing one’s investment portfolio to produce the needed income is just as personal and just as unique. If one wishes to go the product route, then he had better have saved a lot of money and avoided the last-minute downfall. On the other hand, if one goes the route of professional service, then she will be able to navigate life’s ups and downs with far more flexibility. Bear markets are horrible to endure, but they do produce opportunities – even for those about to retire.

Warm regards,

Chuck Osborne, CFA

Managing Director

Chuck Osborne, CFA

Managing Director

“‘Be careful,’ Jesus said to them.‘Be on your guard against the yeast of the Pharisees and Sadducees.’”

~ Matthew 16:6

This is one of my favorite Bible verses. (That may seem strange as I am not sure how many top-10 lists this makes.) For those who have not studied the Bible, one is often shocked by how much of our language and culture come from that one book.

How many Matthews, Marks, Lukes, and Johns do you know? You can’t be Better than Ezra if you don’t know Ezra. How can you Turn! Turn! Turn! with The Byrds if you have never read Ecclesiastes? We know a young family who recently named their baby boy Jude, and a friend speculated they named him after Jude Law. Perhaps, but my guess is it comes from “Jude, a servant of Jesus Christ and a brother of James”, as the author of the book of Jude described himself. If it was Jude Law, I’d wager that his mother probably knew the origin, and I am almost certain the Beatles did too.

Stepping outside of the Bible for the spirit of that verse, how about the famous basketball coach John Wooden? “It’s the little details that are vital. Little things make big things happen.” Yeast is a very small thing, but the difference it makes in bread is huge.

Earlier this year, a prospective institutional client asked me what Iron Capital does to protect retirement plan sponsors from liability. This is a reasonable concern, as many employers have been sued over their retirement plans. First: everything Iron Capital does for plan sponsors helps protect them from any possible liability. However, the way the question was asked sparked something in me; for the lack of a better term, it was a yeast moment here in Iron Capital’s 20th year.

Years ago, I was at a basketball game with a close acquaintance who was on the investment committee for a local employer I was interested in pursuing as a client. While we watched the game, I let him know how Iron Capital was different than other firms. We discussed our investment process and the success we had building retirement plans. He told me something I’ll never forget. “Chuck, I’m impressed with what you all have done, and I would be all for hiring you, but my company isn’t interested in having the best retirement plan around. We just want someone big whom we can sue if things go wrong.” In other words, what are you going to do to protect us from our liability?

That time I just thanked him for his warning and moved on, but earlier this year something struck me: There is very little difference between doing the right thing for plan participants and covering one’s behind – DTRT or CYA? The difference in action is no bigger than a single grain of yeast, but oh my what a difference it makes in outcomes.

We pride ourselves on our ability to select investment managers for retirement plans. We track our results, and although it is hard to compare to others as there are no databases, I would wager we are among the best. Over the 10-year period that ended June 30, 2023 (September 30 data not yet available), the funds we have had in our client plans for 10 years or longer have delivered an excess return of 0.82 percent per year; 64.3 percent of these funds outperformed their benchmark by an average of 1.56 percent per year. The funds that underperformed (which includes all index funds, as they underperform by design) did so by an average of 0.51 percent. When blended, we get an average of 0.82 percent excess return. Let’s put that in perspective: T. Rowe Price recently published research showing that a 0.50 percent excess return over the life of a 401(k) participant equates to an additional five years of retirement income.

We are proud of that achievement, but how did we do it? There are many factors, but one of the most important is that we are patient with good managers when they go through bad periods. We don’t track the data this way, but I would wager that every one of the managers who outperformed over that 10-year period has underperformed during some shorter-term period along the way. That puts tension on DTRT vs. CYA.

I cannot count how many difficult conversations I have had with clients over the years about this. When a manager in a plan underperforms, the easiest thing for a consultant like me to do is to go to the meeting, point to the underperformance, and announce that we are replacing the manager. No one would ever argue; the manager is underperforming, and we are “doing something,” and doing something makes clients happy. What we are doing is CYA. Clients don’t like underperforming investment managers, and firing them as soon as possible leads to happy meetings.

However, it doesn’t lead to good results for participants. If the manager in question was good to begin with, then she will likely rebound and do well coming out of the short period of underperformance. Meanwhile, the managers that look good right now probably look good because they manage money in a different way.

Take Iron Capital as an example. In 2022, we experienced a bear market in stocks and a historic bond selloff simultaneously, and the more growth- oriented stocks dropped the most. Our aggressive growth stock strategy underperformed, our core stock strategy outperformed, and our income strategy outperformed dramatically. In 2023, the market has rebounded somewhat, but almost all of those returns have come from a small number of very aggressive growth stocks. This year our aggressive growth strategy is doing well, our core stock strategy is underperforming, and our income strategy is suffering.

We are the same team managing these same strategies. These short-term results are not due to us being really bad at growth investing and really great at income investing in 2022 and then flipping a switch and becoming really bad at income investing and awesome at growth investing in 2023. We are just in a different market environment. An investor can be successful over the long term with either strategy if she sticks to her strategy; the investors who lose are the ones who keep switching strategies. The industry term for this is whipsawing. If an investor switches from growth to income at the end of 2022 just to be in the popular place, he now has been in the worst place twice in a row. Some may believe that they could do the opposite, but history tells us that is a fool’s errand.

The phenomenon of whipsawing means that a retirement plan adviser who is in CYA mode and goes into the meeting with the client promising to switch out managers almost always whipsaws the participants. At the end of ten years, they can’t show the results we have, because they have never given a manager 10 years. They have, however, had peaceful meetings with retirement plan committees and always been able to point to high performance on performance reports; but the performance on the reports is all from before the manager was in the plan, so no participant experienced those good results. However, to my knowledge to-date, no employer has ever been sued for switching out managers too frequently. From a CYA perspective, success has been achieved.

How is it different when the motivation is DTRT? The DTRT adviser gets to take it on the chin. He gets yelled at, a lot (trust me on this). How could you keep this manager in the plan? It would be so much easier to say, “Sir, yes Sir, we will replace him right away. Would you like to come to our annual boondoggle, I mean plan sponsor conference?” But the DTRT adviser understands that the client isn’t always right. If she were, then she wouldn’t need an adviser. The DTRT adviser is willing to have difficult conversations because what motivates her is delivering results for participants.

This doesn’t mean there will never be any turnover in managers. Sometimes replacement is the only option. However, replacement should be done when and only when there is a reasonably high probability that the new manger will do better going forward. It is easy to find someone who did better in the past, but picking someone who will do better going forward is far more challenging. The CYA adviser doesn’t really care about that, because he will just replace the new guy as soon as he stumbles.

The CYA adviser is also going to be laser focused on fees…all the fees except his of course. CYA is expensive. This is not to say the DTRT adviser won’t focus on fees; after all, fees are a hurdle that must be overcome. If the T. Rowe Price research is correct and an additional 0.50 percent means an additional five years in retirement income, then every fraction of a percent matters. Here is another grain of yeast: fees matter, but to the DTRT adviser, value matters more. Fees are easy to poke at, but understanding what value is being driven by those fees is much harder. When the CYA adviser continually whipsaws participants then the value add is negative, so any fee at all just adds insult to injury. However, when a DTRT adviser adds 0.82 percent of value a year for ten years net of fees, then the value proposition matters more than just the fee level.

Of course, past performance is no guarantee for future results; just because we have done it in the past doesn’t mean we can keep doing it. That is true, and I would be less than honest if I ever guaranteed otherwise. What I can tell you is that the 10-year period I discuss here is the worst we have done since we have been tracking this statistic. I can promise that we are our own worst critics, and I am more than willing to get yelled at in client meetings because the client is only expressing emotions that we have already dealt with internally. I can also promise that we will continue to always strive to do the right thing, which is what has driven our success in the past.

Does DTRT provide as much protection as CYA? I don’t know, but I do know that in Iron Capital’s 20-year history, none of our clients has ever been sued for mismanagement of the retirement plan. Maybe that is because of our success at selecting good managers and building good plans, but I suspect there is more to it: DTRT advisers usually end up working with employers who themselves are not trying to just CYA, but who actually care about their employees. That also might be hard to differentiate as salaries and benefits are largely driven by market forces and regulation, so CYA and DTRT might not look that different on the surface. It shows in the culture.

Years ago, I pointed out that a large portion of Warren Buffett’s success was because he essentially fired his clients by shutting down the fund he originally ran and using Berkshire Hathaway as his vehicle for investing. The alternative to that is to have really good clients. Iron Capital owes much of its success to the quality of its clients – all of our clients, but especially the plan sponsor clients. We are fortunate to work with companies that truly care about their people. It shows in all the little things, which is why we must beware of the yeast. It is the little things that make the big things happen.

Warm regards,

Chuck Osborne, CFA

Managing Director

~Beware of Yeast

We have just experienced one of the strangest quarters that I can remember. At the beginning of June, Goldman Sachs research indicated that all of the return for the S&P 500 year-to- date through May was attributed to just seven stocks; the other 493 stocks in the S&P 500 have an average return of zero, nada, zilch. How did that happen?

Let’s start with some history. We are going back all the way to 2022…which sounds silly in most conversations, but stock market participants are famous for their extraordinarily short memories. After a decade of technology stocks dominating all the returns in the stock market, the rest of the market finally got some revenge in 2022. Value investors outperformed their growth colleagues for the first time in a long time and the gap was large in the final quarter of 2022. The Russell 1000 Value Index was up 12.42 percent, while the Russell 1000 Growth Index was up only 2.2 percent.

The new year began with growth stocks making a comeback: In the firstquarter of 2023, the growth index was up

14.37 percent, with the value index up just 1.01 percent. At first this was just the normal back-and-forth of the markets. We often refer to a phenomenon known as reversion to the mean – meaning that stock investment results tend to move toward the long-term averages. If they get well above the average they tend to drop, and if they get too far below the averages, they tend to rise. That explains one good quarter for the growth stocks, but as we moved into the month of May, something else started to take over – something that is certainly artificial, but is it intelligent?

Time will tell as far as stock prices go, but there is no doubt that artificial intelligence (AI) has dominated the stock market in 2023. The poster child for this phenomenon has been Nvidia; the stock has risen 189 percent in 2023. Before we get too excited, remember one thing pundits never bring up: Nvidia stock went from $326.76 in November 2021 to $121.39 in September 2022. The stock is up approximately 30 percent from its high in late 2021, which is a solid two-year return, but not as exciting as the “up 200 percent” we hear about.

The rebound in Nvidia stock has to do with generative AI such as ChatGPT. These are computer algorithms that can create new content. It is a breakthrough in computer technology, and the long- term potential is tremendous. Experts in the field have suggested that AI will be bigger than the internet, and there is already fear of AI coming for all of our jobs. The machines will take over just like they did in “2001: A Space Odyssey,” or “The Terminator,” or “The Matrix,” or “I, Robot” … you understand, it has been a thing for a while now.

Nvidia is the leader in designing chips used in Graphic Processing Units (GPU), which are key to the computer power necessary for AI. Microsoft has also benefited as they are a leader in the cloud and have announced a partnership with OpenAI, the maker of ChatGPT. Additionally, some well-known tech companies have the potential to benefit: Meta (Facebook’s parent company), Alphabet (Google’s parent company), Amazon, Apple, and Tesla are all believed to be beneficiaries of AI’s potential. Combined with Nvidia, they have been dubbed the “Magnificent Seven.”

It is these seven stocks that have dominated the returns this year. They completely skew the valuation of the market and the market’s return, and it is these that pundits are really talking about when they ask if the market can continue to rally. Let’s address them specifically.

I am no technology expert, but I do know a little about how the market reacts to technological breakthroughs. The market response is a phenomenon called the Gartner Hype Cycle: It begins with a technological trigger – the breakthrough itself kicks things off. We then move to the peak of inflated expectations, and early publicity leads to grossly exaggerated claims of potential. Then, we enter the trough of disillusionment – technology has never adapted as quickly as the zealots believe it will, and when the fantastic predictions fail to immediately materialize, then bubbles burst and stocks plummet.

That leads to the slope of enlightenment: Technology has never adapted as quickly as zealots believe, but it has adapted faster than naysayers would suggest. People start to see realistic applications. These realistic applications eventually lead to the plateau of productivity, in which the new technology is being used to make our lives easier – not as first imagined, but in real ways nonetheless.

AI is currently in the peak of inflated expectations. Nvidia’s stock is selling at a price-to-earnings (P/E) ratio of 215, so a speculator in Nvidia’s stock is paying $215 for every $1 in earnings. That is not sustainable, but does that mean the market will come crashing down?

No, it does not. There are 493 stocks in the S&P 500 alone that have been neglected thus far in 2023. The excitement over AI is understandable, but it is only part of the market story thus far in 2023. The other part remains the insistence by many pundits that the recession they said would be here by now is just delayed, as opposed to them just being wrong. The theory goes that the never-arriving recession is right around the corner and therefore stocks will get beat up, so let’s get ahead of it and beat them up now…except for the Magnificent Seven, because with the power of AI these companies will be able to grow regardless of what is happening in the economy. That is true and was certainly the case in the aftermath of the Great Recession. Then it was the FANG stocks (Facebook, Amazon, Netflix, and Google) that held up the market. However, the idea that we are heading into a recession today has thus far been wrong. At some point, reasonable people must admit their mistake.

Let’s play devil’s advocate just for a second: Let us pretend that the people who have been saying we are heading into a recession for the last year and a half are actually correct, so the recession arrives and the AI companies are the only ones growing. So far so good, but what about the stocks that usually hold up in recessions? Defensive stocks like utilities? Duke Energy’s stock is down 13 percent year to date. This makes no sense for two reasons: First, utilities should hold up well in a recession, and secondly and perhaps more importantly, what do GPUs (graphic processing units), cloud computing, and electric cars all have in common, besides AI? They all use enormous amounts of electricity. What does Duke Energy sell? Oh yeah, electricity. In what world can Tesla and Nvidia thrive but utilities suffer? That world does not exist.

Maybe utilities shouldn’t have been beaten up like they have been this year, but when that recession we keep hearing about finally comes, stock valuations must come down. Fair enough, but the index valuations are now completely skewed by the Magnificent Seven. One of the ways Iron Capital looks at valuations is to compare the valuations of different asset classes, and then comparing them. The valuation spread, or difference, between domestic stocks and international stocks is currently at a two standard deviation level. In plain English – the difference between international stocks and domestic stocks is larger than it normally is by an unusual amount … so unusual that this happens less than 5 percent of the time. Nvidia may be selling at 215 times, but the French energy company Total Energies is selling at only 6 times. This is unbelievably inexpensive.

So, what does all this mean? It means the headline story of the first six months of 2023 is misleading. When pundits say the market is up, they are really only talking about seven stocks in the S&P 500. When they say it is expensive, they are really only talking about seven stocks. When they say it can’t continue, they are right – if they mean those seven stocks. The other 493, on the other hand, are poised to catch up.

We are optimistic about the rest of 2023, but it can’t look like the first half. First, the doomsayers need to admit they are wrong: We are not heading into a recession because interest rates are returning to normal levels. Second, AI may indeed be bigger than the internet one day, but that day is a lot farther away than the zealots believe…it is also closer than the naysayers might think, but it isn’t here yet.

Before this little detour into insanity, we saw the markets rotating to value, small and international. That remains the long-term trend, and one six-month tease doesn’t change it. That rotation has legs, and the power of both momentum and valuation. We just need patience. Prudent investing pays off in the long run, but it does require patience.

Warm regards,

Chuck Osborne, CFA

Managing Director

July 2023

~Artificial Distribution

“Are we heading into a recession?”

This is the number-one question I have been getting from clients recently. I answer with a question: How is your business? The answers vary, even inside the same company.

One of our long-term clients is primarily in the transportation business. They have other businesses as well, including a few very good restaurants, but their main business is helping goods get into our harbors, off of ships, and up rivers. They have several locations around the country, and we get to go to all of them. I shouldn’t say this on the record because now they will be on to me, but casual conversations with this client have an impact on our view of the economy. They are on the front line. I almost laugh when they ask for my view – I sit in an office reading reports. These folks are moving a significant portion of everything you buy. They will know long before I do whether the economy is slowing down.

Just a few weeks ago I was visiting their Norfolk, VA, location. Someone there asked me about the economy, and I replied by asking about their business. “We are busy,” was the response. Last year was a record year and they are expecting it to be just a little higher this year. That is an encouraging sign, but is it universal?

A few weeks before that visit I was talking to the same company’s CFO. When I asked him how business was going, his response was a little different. He said that when viewing potential mergers or acquisitions, they now had to factor in the cost of capital. In other words, higher interest rates mean that it will cost them more if they decide to purchase another company. That may mean fewer business deals this year. That isn’t encouraging.

Meanwhile, one of my colleagues visited the same client’s New Orleans location. When he asked how their business was going, they said it was good, but some of their clients are seeing a slowdown because they used to bring grain from Russia, which now isn’t happening because of the war in Ukraine. That is interesting.

The same client, yet three different takes on the economy. I have also gone on record saying that I believe the power of the Fed over the real economy is hugely overrated. I still believe that, and I still believe that Wall Street and economists in general remain overly pessimistic. How do we make sense of these mixed messages?

Albert Einstein famously said, “If you can’t explain it simply, you don’t understand it well enough.” I believe he is correct, but it goes further. Most experts can’t explain things clearly because they are more concerned with being considered an expert than communicating clearly to the everyday person. In other words, their egos get in the way. They insist on peppering their speech with jargon, or worse yet, acronyms. As a result, in my opinion, they often lose sight of the most basic fundamental understanding of what is actually happening.

The experts cite past data showing that when the Fed raises interest rates, the economy goes into a recession. They get so focused on analyzing data that they forget to ask the most fundamental questions: Why? What is really happening?

Raising interest rates impacts just one thing: the cost of borrowing money. That is what interest rates are – they are the cost of borrowing money. When one purchases a house, she usually borrows the money in the form of a mortgage. That mortgage, like all loans, has an interest rate tied to it, and the interest must be paid. The higher the interest rate, the higher the monthly payment.

However, that same consumer, if she is being responsible, doesn’t borrow money to buy groceries, clothes, or any other day-to-day item. Most of the goods we buy do not require loans, so interest rates don’t have an impact. Likewise, a company will usually borrow money to buy another company, to build a factory, or for any other major business investment. That same company hopefully does not borrow money to hire a new employee, pay their office lease, or any other routine business expense.

Those day-to-day items, which are paid for out of pocket, make up the bulk of economic activity. Roughly 70 percent of our gross domestic product (GDP) is made up of consumer spending. For consumers to spend, all they need is an income source, preferably a job. Companies mostly hire without borrowing and most consumer spending is done without borrowing, so the majority of the economy is not actually impacted by the Fed raising interest rates.

However, there are items that typically require borrowing, and these items will be impacted by higher interest rates. For the consumer, those are primarily automobiles and houses. For companies, the biggest items that require borrowing in our current economy would be other companies – mergers and acquisitions. One of the primary drivers of an individual company’s growth is its ability to purchase competitors and/or suppliers. Occasionally they will even purchase a completely unrelated business.

Mergers and acquisitions also fuel much of the financial universe. Investment bankers are the financial professionals who help negotiate and fund mergers and acquisitions. This is a large part of Wall Street’s business, and that is important to understand. Higher interest rates will make it more expensive to buy businesses, just like they make it more expensive to buy houses. That will result in fewer mergers and acquisitions.

How do fewer mergers and acquisitions impact the economy? Buying another company can be of significant benefit to the owners of both companies. The owners of the company being purchased get a big payday, and the owners of the purchaser now own a much larger company. What benefit is this to the economy as a whole? Very little, if any. Economic activity is measured by GDP, which is the gross domestic product – or in plain English, everything that is made and consumed in the country. The two companies produced a certain amount of goods. When they become one company, they still produce roughly the same amount of goods. There may be some efficiencies gained that boost production on the margin, but that also comes with the fact that two companies becoming one usually involves some people losing their jobs. This activity is great for owners and for Wall Street, but it doesn’t really help the economy.

Today we seem to be in the mirror image of what occurred in The Great Recession following the 2008 financial crisis. For nearly 8 years after that crisis, we kept hearing from Wall Street and economists that growth was right around the corner. Yet years after the crisis ended surveys suggested that most people still thought we were in a recession. Why? At that time the Fed aggressively reduced interest rates, eventually all the way to zero. Money was practically free to borrow.

This spurred a boom in housing and in mergers and acquisitions – big purchases that require borrowing. Housing will stimulate the economy, but as we discussed, mergers and acquisitions don’t really add to the economy as a whole. So, while business owners and financial professionals benefited from free borrowing, the bulk of the economy just didn’t grow. This led to an environment where economic growth kept disappointing the financial experts.

Today interest rates are rising, and the same financial experts who kept predicting growth that didn’t come a decade ago are predicting a recession that has yet to show up now. We can see why Fed policy impacts the owner class and financial professionals much more than it impacts the economy as a whole, but why can’t the economists see it? My theory is that it is human nature to see the world through one’s own view. In my experience, this happens regardless of one’s level of sophistication. We all tend to believe that people think the way we do, and that what we are experiencing is what everyone else is experiencing.

When interest rates are very low, things like mergers and acquisitions happen easily, benefitting business owners and financial firms who are the primary employers of economists outside universities. Their economic lives are good, so their view of the economy is positive. When interest rates are higher, things like mergers and acquisitions become harder, and that hurts business owners and financial firms. Their economic lives are in recession, so their view of the economy is negative.

Meanwhile, the vast majority of consumers are just going on with their lives. When there are a lot of mergers and acquisitions happening, rank-and-file employees are under stress. Things at work are changing and some are likely to lose their jobs. They may even curtail their spending. When interest rates are high, there is less change at work. The consumer hangs in there.

This explains a great deal about why, in the last 20 years or so of record-low interest rates, the gains in our economy have skewed to the owner class and financial professionals. There has been disappointing overall growth and an increase in inequality. It also explains our current situation, and the different stories from our client in the field and the chief financial officer.

But what about the slowdown driven by government sanctions on Russia? Economists love to analyze interest rates and tax rates because these are numbers and can be quantified. Government regulation, on the other hand, cannot be quantified easily, if at all. Sanctions against Russia are a great example: As long as our government says no to Russian grain, it will not come here. It doesn’t matter how much demand there is for grain, or what interest rates are. This is a structural barrier that cannot be overcome. Only the government can remove that barrier if they so choose.

I do want to be clear: Sanctioning Russia may very well be the right thing to do, but that is a political judgment and not an economic judgment. These sanctions, like all government regulations, create structural barriers to economic activity that cannot be overcome by attempting to stimulate the economy. This is important to understand, because over the last 23 years, there has been only one period of time when economic benefits were flowing to rank-and-file workers faster than to owners: that was in 2017-2020, when we saw the first decline in regulation since the 1990s.

When structural barriers are removed, then we can get real economic growth, which benefits everyone, instead of financial engineering, which only benefits the few. Today we are going in the opposite direction, which does not bode well for the longer term.

In the meantime, the economy is hanging in there better than most experts suggest. This is because rising interest rates are not actually stopping consumers from living their daily lives; they are, however, making it harder for mergers and acquisitions. They triggered a bear market last year.

This all means that those experts who are predicting doom and gloom are themselves experiencing a personal economic recession, coloring the lens through which they make their projections. What they are really saying is that they are being hurt by this environment and therefore they assume everyone else will be hurt as well. It is understandable, but it may not work out that way. We maintain our view that we will either escape a recession all together or have a very mild one. We are not basing that on our business, but on feedback we get from others.

So, how is your business?

Warm regards,

Chuck Osborne, CFA

Managing Director

~How’s Business?

We have wrapped up one of the strangest years in the financial markets in my memory. It feels like we are living in Bizarro World. For those who did not grow up with “Superman” comics, Bizarro World was a planet where everything was bizarre.

We had high inflation, which we (and every other analyst I know) saw coming, yet somehow the Fed did not. We had two quarters in a row of real GDP declines, which has always been the practical definition of a recession, but pundits insist that it wasn’t a recession this time. We experienced the worst stock market since 2008, and to add some salt to that wound, the bond market collapsed. The U.S. Aggregate Bond Index goes back to 1977, and in those 45 years, bond prices have been down only five times. The worst decline before 2022 was in 1994 with a 2.9 percent drop; In 2022, bonds dropped 13.01 percent.

The bond market carnage at least makes sense, as the big issue in 2022 was inflation. Inflation causes interest rates to rise, which the Fed’s actions accelerated. The stock market, however, is a more nuanced story. It would be easy to relate the drop directly to inflation, and inflation can certainly hurt some companies; however, inflation actually helps more companies than it hurts, at least on paper, as stated earnings get inflated with everything else. Energy companies are a great example of this and were the best place to be last year.

Stocks dropped because the majority opinion of market participants is that the Fed raising rates will cause a recession. In the 30-plus years I have been in this business, I do not recall a time when so many were so convinced that a recession was inevitable… which is precisely why I doubt a severe recession will occur this year. Perhaps I am being a bit of a wimp in adding the caveat of “severe” here, but stay with me.

Before I explain our thought process, it would be good to discuss what causes recessions in the first place. The economy flows in a way not dissimilar to nature: There are seasons, and spring leads to summer, which gives way to fall, and eventually winter. Winter, with all of its brutality, gives birth to a new spring. Trees grow, they mature, then fade and die, and in doing so, fertilize the soil for a new tree.

Similarly, a business also has a spring, summer, fall and winter. The four largest companies in America today are Apple, Microsoft, Alphabet, and Amazon. Apple was founded in 1976 and Microsoft in 1975. Alphabet was founded in 2015 as the parent of Google, which was founded in 1998. Amazon was founded in 1994. The four largest companies in the U.S. today did not exist when I was born, and two of those four did not exist when I graduated from college. How about you?

Nature has its seasons, and the economy has the business cycle. The cycle starts with new growth, new ideas, and new products. It grows into a flourishing summer, and when all looks positive, it then matures into fall and finally dies in winter.

That death brings forth new life, and the cycle repeats. This is the life of a company, and when we combine all the companies that currently exist, we get an economy. The difference between nature and the business cycle is human psychology.

The great sin of humankind is the thought that we can control things which cannot be controlled. In the Abrahamic traditions, Adam and Eve brought sin into the world when they ate the fruit of the tree of knowledge in order to be like God. In the Eastern traditions, they speak of having to give up the illusion of control. The ancient philosophers warned of hubris. This is a universal truth, and a bedrock of every tradition that has stood the test of time.

This manifests itself in the business cycle as companies experience the summer of their existence. We start our company selling widgets; our widgets are better than any widget that has previously existed, but in our spring we must overcome the newness. We must get our message out, then scale our production to meet the growing demand. If we survive this season, eventually we enter summer. Growth comes easily. We are no longer a startup but the leader of our industry. Demand is sky-high, manufacturing has been optimized, and profits flow.

If we were animals, our instinct would be to know that fall is coming with winter after that. We would prepare for our survival. But we are not animals, we are human beings, and we constantly believe that summer will last forever. At the moment when we should be storing up the fat for winter, we decide to expand instead. We overreach, and this brings on the fall.

Fall is not that bad. The colors are beautiful. It may start to get a little chilly, but it is nothing a sweater won’t fix. For our business we become a cash cow. Growth in demand has fallen, but we have become very efficient at making our widgets and they are more profitable than ever. We may be selling fewer of them, but the increased profit keeps our illusion of summer alive. While even the squirrels are wise enough to store all the falling nuts, we convince ourselves that we are still in control.

Then winter hits. In nature the animals hibernate and live off their fat stores, but our business was running very thin. We must take drastic measures. Payrolls slashed and factories shut down. We have brought on a recession. When recessions hit the unprepared, cuts have to be made. Like trees falling in the forest, those cuts lead to new growth.

We had severe recessions in the 1970s, when technology giants like IBM and Hewlitt Packard had to lay off employees – employees who would then take a chance to work for inspired startups named Microsoft and Apple. Twenty years later, a savings and loan crisis caused a recession and companies started trimming the bloat that had built up in the booming 1980s. Those trimmed workers staffed internet startups such as Google and Amazon.

Winter brings forth spring, but with all due respect, there is no cliché about people retiring to Minnesota. People retire to places like Florida because as a whole we prefer summer to winter. Of course, the four seasons take place in one year, while the business cycle historically took place over a five-year period. Macroeconomists have searched for a way to stop winter from coming. John Maynard Keynes theorized that we could stop it by having the government spend more when things began to slow.

Keynes’s theories dominated the period that led to the high inflation, high unemployment, and low growth of the 1970s. It was a disaster. Milton Friedman thought it better to use monetary policy – the Fed could keep us from recession by manipulating interest rates. As a result, we have successfully lengthened the business cycle from five years to a decade or more. The good news is that winter takes longer to come; the bad news is that the winters have become severe – the tech bubble, real estate bubble, and financial crisis. The more people become convinced that “this time it is different” and winter won’t come after all, the worse the impact of the inevitable change of season will be.

Why is that? Winter is fairly mild here in Atlanta, but those who have experienced a Southern winter often speak of it feeling colder. I blame the humidity. Years ago, I mentioned this to my boss at the time. He was from Detroit and knew a thing or two about winters. He just looked at me and said, “That is because you people don’t wear coats.” He was right, and I have forsaken my Southern roots ever since and brought out the coats anytime it gets cool outside.

This brings me back to my somewhat gutless prediction: I believe we may escape a recession in 2023, or if we do not escape entirely, that the recession will be very mild. I say this because everyone seems so convinced that winter is coming that they are actually preparing for it. Recessions happen, especially severe ones, because we constantly believe they won’t come and therefore overextend ourselves.

We are not overextended; this may be the silver lining in the very dark cloud which was our reaction to the COVID- 19 pandemic. We had not had a recession since the financial crisis of 2008, so we were overdue, but as we entered 2020, all was well economically speaking. We were experiencing the best economy we had seen since the 1980s and 1990s, then we decided to shut the world down in an effort to control the path of a virus. (There is that control thing again.) So, recession started.

We were rebounding from that self-inflicted recession when we decided to reverse course on the lessons of the 1970s and once again embrace the inflation-causing Keynesian fiscal policies of the past, which has landed us where we are today. We are less than three years removed from the last recession, and we are nowhere near the end of a new business cycle; if anything, we are closer to the beginning. This is not the environment which leads to severe recessions.

That doesn’t mean we might not have a slowdown or even mild recession. This can simply be a self-fulfilling prophecy: If everyone slows down to stock up for winter, then economic activity will decrease. Additionally, when we speak of recession, we are referring to the economy as a whole. There are always exceptions. Energy companies have been going gangbusters, but they did horribly for the decade before when technology companies thrived.

Today the economy as a whole may be hanging in there, but the mortgage business is hurting severely and certainly experiencing a recession-like environment. Any industry that is tied to interest rates or financial markets has been hurt. This is balanced, however, with others doing well. One tree falling does not mean the forest is dying.

Critics of capitalism never seem to grasp this. There is a growing movement among some today who suggest that our society is too focused on growth; this is incredibly misguided. There are only two states of being: growth and decay. If we stop growing, then we are decaying. The capitalism critics fundamentally misunderstand what growth of the economy means; they seemingly think of the economy as a tree and even use analogies of trees not being able to grow to the sky. The economy is not a tree, but a forest. The forest can grow forever without ever getting bigger or using up more resources, because the forest hosts new growth along with decay.

The four largest companies today did not exist when I was born. Two of them didn’t exist when I graduated from college. The four largest when I was born were General Motors, Exxon, Ford, and General Electric. They all still exist today, although General Motors wouldn’t if the government had not bailed them out during the financial crisis. All are mere shadows of what they once were, all in the fall of their existence. Who knows what the largest companies will be years from now. Change is inevitable. Recessions are as natural as winter itself; perhaps we would be better off if we stopped trying to control them out of existence.

Warm regards,

Chuck Osborne, CFA

Managing Director

~Inevitable

Myths die hard. For as long as I can remember, there has been a myth that investors must reduce their exposure to stocks and increase their exposure to bonds as they approach retirement. This advice is based on the fallacy that if one is exposed to the stock market and we have a bear market (as we do today) at or close to one’s retirement, then his retirement will be forever impacted. He will have to live on less and suffer for his bad timing.

That is wrong. It is wrong in lots of ways, but most importantly it ignores a far greater risk: outliving one’s resources. In the 30 years I have been in the investment business, primarily focused on retirement, I have seen four huge mistakes that need to be avoided at all costs. The first is taking too much risk when one is young, then panicking and selling everything during a bear market. We talk about this often.

The second is retiring without a plan. I am not talking about a financial plan; I mean an action plan. What are you going to do that will take up your time and fill your life with meaning? If you do not know the answer to that question, then you are not ready to retire. Vacations are great, but they are largely great because they are short. If one retires at age 65 today, then she is likely to be in retirement for 25 or 30 years. One can only play so much pickleball. She had better have a plan as to what will keep her active and engaged with others.

The third mistake is outliving one’s health. Modern medicine is designed to keep one from dying, and they have gotten really good at it. That, however, is not the same as living. The more I deal with retirees, the less I care how long I live. I just want to really live right up until the end. Even if you have never exercised in your life up to retirement, you had better start, because your ability to physically function is a use-it-or-lose-it skill.

The fourth mistake is the one we will deal with in this article: becoming too conservative at or in the decade or so before retirement. This leads to outliving one’s resources, and if there is anything as horrible as outliving one’s health, this is it. The risk of outliving one’s resources is the risk that investors should think about the most. It dwarfs the risk of market volatility, yet that is what most people think of as risk. Most people look at what has happened to the market this year and think, “This is risk; this is the scary part.”

It is human nature. We know better, but it is difficult to see the current value of one’s investments drop and not be anxious about it. That is a normal reaction, but we have to remind ourselves that this is part of the cycle of life. We see ups and downs, and the ups will outweigh the downs over time as long as we stay the course. Time is on our side. Since 1926, the S&P 500 has been up 72 percent of the time. We get a negative year on average once every four years. This will pass, and the market will go to new highs.

This truth leads to one of the fallacies that causes people to hit the brakes too soon. They say, “If you are young then you have time to recover, but if you are about to retire, then you do not.” Wrong! This is the fallacy of the wrong time horizon. An investor who is investing for her retirement does not have a time horizon that ends on her retirement date; her time horizon is her life expectancy, which today is at least 20 years after retirement. I use 20 because when I was an economics student, we learned that as far as mathematical projections go, 20 years equals infinity. Anything beyond that time period is pure garbage. In our investment policies, the longest time horizon one can have is 20+ years, and one has that time horizon into their 70s.

How did the idea of retirement as an end date ever get started? Unfortunately, that has to do with the evolution of the investment industry and the incredible difficulty the industry has in serving investors through retirement. Many years ago, investors either did it themselves or hired an investment adviser to manage their money for them. Either way, all the actual transactions had to go through a broker. In fact, to simply know what was happening in the market that day one had to go to a “wire house” brokerage firm. These were the large New York-based broker-dealers who would pay the expense of having a wire service run to their regional offices around the country.

These firms had brokers in all of these offices because the only way to transact was in person. Technology has replaced that entire system. If your phone has a cell signal, then you can know what is happening and can trade stocks. In most businesses this would have meant the end of the broker, and in my opinion it should have. However, in the investment business, the broker transformed himself into the financial adviser. The broker’s historical role was that of a salesperson. If his broker-dealer had stock of GE, then he would be selling GE that day. The next day they might have a bond from GM, and he would sell that.

The role has not really changed, but most people today are not interested in paying the high cost of buying a stock or bond from the salesperson when they can do it far more efficiently online. Today the financial adviser sells money management; unfortunately, he isn’t a money manager. However, this works for most money managers, because they frankly are more comfortable looking at spreadsheets than talking to people. They can manage money the way they want and turn it into a product that gets sold by financial advisers, who are generally good with people.

Hence, the money management industry evolved from a service profession to a product manufacturing business. The brokerage business evolved from selling stock and bonds to selling managed products. This is far from ideal in our opinion, but it does work for accumulating resources. The vast majority of the products sold by advisers are geared toward growing one’s investments, so while a truly tailored approach is not possible, it is possible to build a portfolio of products that will grow in value over time.

The problem comes when one retires and transitions to producing income. While everyone who is still in the accumulation phase can be oversimplified as needing to make money, each person in the income phase has a truly unique situation. Designing a product for that is like trying to fit a square peg into a round hole – it simply will not work.

It also leads to the idea that when one retires, she must take all her money and put it into an income-producing product. If one did that, then the balance of the portfolio on the day of retirement becomes extremely important. If the investment industry is just a product-pushing business, then the timing of switching products becomes much more important than it should be.

At Iron Capital, we do not believe that the industry should be about pushing products. We believe it is supposed to be a professional service. As such, we build each income-producing portfolio from the bottom-up, tailored to each client’s needs. Our philosophy is simple: Build a portfolio that generates the income needed while taking as little risk as the market will allow.

We have been in a historically low-interest-rate environment for most of the last 20 years, certainly since the financial crisis in 2008. This hurts most income-focused products because they primarily invest in bonds. Bonds, after all, are simply loans. The loans are paid back plus interest, which produces income. The industry has really struggled in trying to solve the retirement income puzzle in this environment. For the most part, they just gave up and started telling their clients that they would have to live on less.

Article after article preached the demise of the so-called 4 percent rule – the “rule” that one could only take 4 percent of their portfolio as income if they wished to preserve the capital. In the meantime, most of our clients need closer to 6 percent. The product-based solutions are no solution at all. We have delivered the income our clients need by taking the best income sources available at the time. For most of the last 20 years that has meant dividend-paying stocks, preferred stocks, and higher-yielding bonds.

The good news is that while we have more in stock, the stocks we were investing in for these clients are more conservative. They tend to hold up extremely well during market downturns. The one exception to that rule was the Covid shutdown. These conservative companies that pay dividends tend to do well in thick or thin, but not when the government says you have to shut down. So, what did we do?

We put enough in safe places to pay the income needs for a few years, and then took advantage of the silver lining of the downturn. Every bear market creates opportunity. We took advantage of that opportunity to rebuild our client’s income portfolios. This is also what one should do when retiring in, or shortly after, a bear market.

When producing the needed income is a professional service and not a product, one gains flexibility. There is no need to have a one-time flip of the switch; the transition into retirement is exactly that – a transition. There is no rush, as we are going to be managing the income production for 20 to 30 years, if not longer. There is no need for a bear market at one’s retirement to be any different than a bear market at any other time.

Today we are in a bear market, and it is creating opportunities. For the income-needing client, those opportunities are now in bonds. For the first time in a very long time, bonds are paying enough interest to be a meaningful portion of an income strategy. This, however, is not going to help the product pushers. Bonds are simple: One loans his money to a company or government, and the borrower promises to pay it back plus interest. If one buys a bond, then she will get interest payments, and at maturity, the return of her principal. There is a risk that a borrower will not be able to pay it back, but that risk can be judged up front.

Bond funds, i.e. the products, do not work that way. What one is really doing is buying shares in a mutual fund. The fund then invests in bonds. Should interest rates rise further, the bonds will lose value in the market. A bondholder who isn’t selling doesn’t care, because she will continue to get what she agreed to from the beginning. The bond fund, however, will lose value. It does not behave like an actual bond; it behaves like a mutual fund that happens to invest in securities with lower return potential.

Retirement is a personal experience. It is a stage of life, not something one buys from a store. Managing one’s investment portfolio to produce the needed income is just as personal and just as unique. If one wishes to go the product route, then he had better have saved a lot of money and avoided the last-minute downfall. On the other hand, if one goes the route of professional service, then she will be able to navigate life’s ups and downs with far more flexibility. Bear markets are horrible to endure, but they do produce opportunities – even for those about to retire.

Warm regards,

Chuck Osborne, CFA

Managing Director

~Retiring in A Bear Market